As somebody with an entrepreneurial spirit, you’re passionate about providing your product or service to the world.

Chances are that you’re not so passionate about the accounting and administrative side of your business, though.

Unless you come from a financial background, it might feel like you’re reading another language when you look through financial statements.

Understanding the basics of your company’s financial statements is critical to making better decisions for your business, though. So it’s important that you learn how to read them.

This article will explain how to read a profit and loss statement. It’s one of the most important ways to gauge the overall financial health of your company at a quick glance.

What is a profit and loss statement?

A profit and loss statement is one of the most important financial statements for your business.

It’s also commonly called an income statement.

No matter what you call it, this statement is the one thing that all bankers and investors will want to see when they’re considering offering you a loan.

That’s because a profit and loss statement (P&L) is one of the easiest ways to tell if your company is profitable or not.

The bottom line of your P&L shows your net profit (amount of money you made after all expenses, taxes, and other deductions are taken out).

If the net profit is a positive number, you know the company made money. If it’s a negative number, you can tell the company took a loss during the period.

The profit and loss statement also gives a summary of your business revenues, as well as your expenses and costs.

A strong P&L statement illustrates that your company can make sales, control expenses, and ultimately produce a profit.

There’s always a specific period that a P&L statement covers. Most commonly, this statement will reflect financial information for the fiscal year. But, you could create a statement for any time period you wished to review.

How is a profit and loss statement different from a balance sheet?

Both a P&L statement and a balance sheet display a company’s finances. Creditors and investors use both, but in significantly different ways.

A balance sheet reports assets, liabilities, and equity at a certain point in time. It acts like a snapshot, and provides insight into the finances of a company on a specific date.

A profit and loss statement provides a summary of revenues and expenses incurred over a period of time. A P&L statement may reflect the financials of a company over an entire month, quarter, or year.

There may be significant variation in a company’s finances from day to day. A corporation may pay all of its invoices on one day, and receive a large payment the next.

So a balance sheet can look different from day to day — especially if it’s a smaller company that follows cash accounting (where transactions are only recorded when the cash changes hands).

In this case, a P&L statement can be a better overall representation of a company’s financial health — as long as it captures a long enough period of time to show a true picture.

Since revenues and expenses get reported over a period of time, an annual P&L statement helps smoothes out any daily fluctuations.

This provides creditors and investors with a more accurate picture of how the company is performing.

A P&L statement also helps financial analysts within the company to understand if they can generate more profit by reducing costs, increasing sales, or a combination of the two.

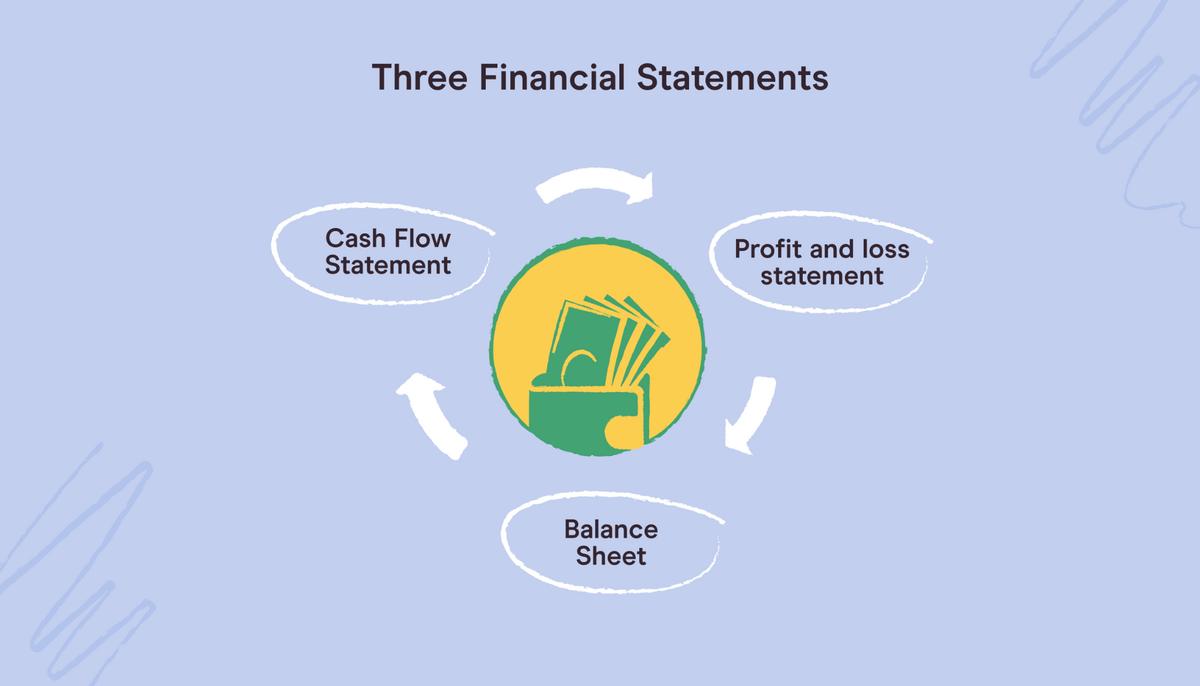

The profit and loss statement is also different from a cash flow statement, which shows actual cash flow in and out of the business during a specific period, and doesn’t follow accrual accounting rules or take into account any non-cash transactions (like reducing the value of assets over time).

What items are shown on a profit and loss statement?

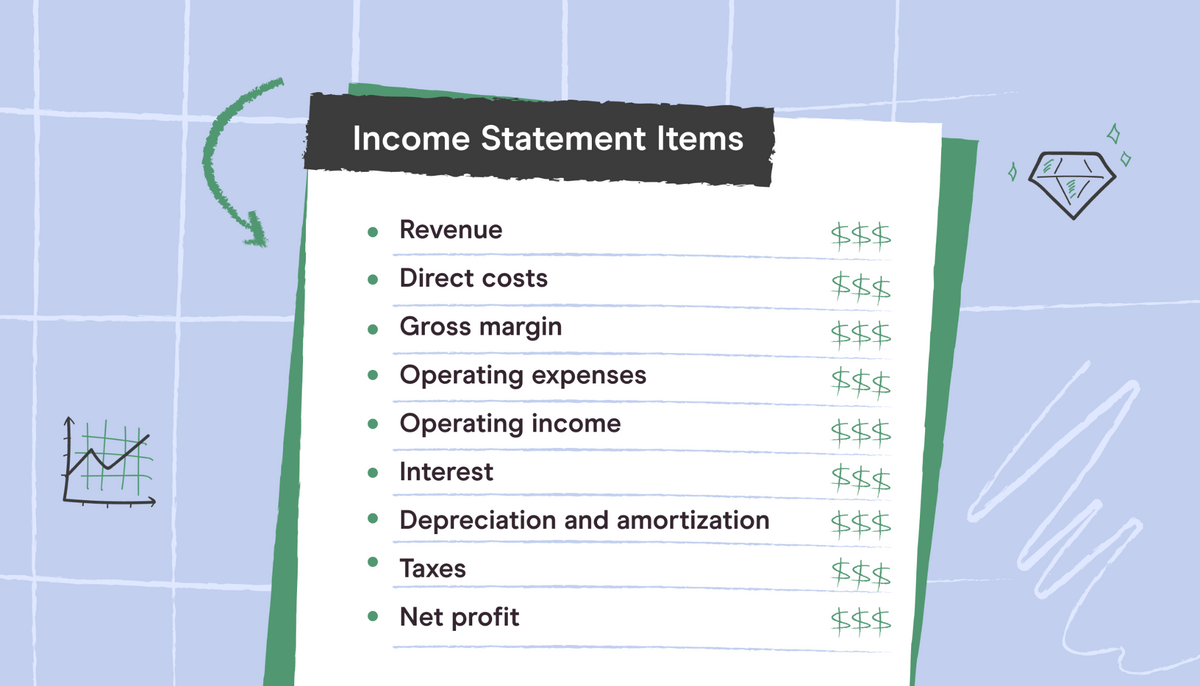

We briefly mentioned earlier that a profit and loss statement summarizes the revenues, expenses, and other costs incurred by a company within a specific period.

However, some of these revenues and expenses are broken down into their own separate line items.

Let’s take a look at nine common items on a P&L statement:

Revenue

Revenue is money brought into the company through making sales to customers.

Sometimes it’s called the “top line” of an income statement, in contrast with the “bottom line,” which refers to net profit.

In a profitable company, revenue will always exceed expenses. You need to have enough revenue coming in to cover all of the company’s costs if you hope to remain solvent.

Some common types of revenue include:

- Sales (from either goods or services)

- Rent revenue

- Dividend revenue

- Interest revenue

Revenue can also be broken out into operating or non-operating revenue.

Operating revenue is the money generated from your main business activities. For example, if you’re a construction company, this is money generated from building structures.

Non-operating revenue is money generated from anything except your day-to-day activities, like earning dividends on your investments.

Both for-profit and not-for-profit companies will have an income statement, and both will list revenue. However, in a non-profit, your revenues will typically be money raised in the form of donations and fundraising.

Direct costs

A direct cost is any expense that you incur when providing your services or making your products. They’re also referred to as cost of goods sold (COGS).

For a company that makes kitchen cabinets, a direct cost would be items like wood, nails, and glue. If you have hourly employees building the cabinets, the cost for their construction time may also be included here.

It’s important to note that we don’t include things like employee salaries or marketing in direct costs. Those will be accounted for later.

Direct costs are only things that directly go into making your product, or get consumed in the process.

Some companies like a legal firm or consulting firm may have very low direct costs. Aside from some printing and photocopying, they’re mostly selling knowledge, so their direct costs are low.

Companies that manufacture physical products will tend to have higher direct costs.

Gross margin

Gross margin (aka gross profit) shows how much money is left over after you’ve used your revenue to cover all of your direct costs.

Total revenue – Cost of goods sold = Gross margin

For example, if you buy a bathtub for $200 and sell it for $500, then your gross margin would be $300.

The higher your gross margin is, the better. A high gross margin means that it doesn’t cost you much to deliver your product or service, and you keep most of the money from each sale.

Operating expenses

Operating expenses are most other costs that might come to mind, which aren’t included as direct costs (or cost of goods sold).

An operating expense is something like employee salaries, marketing expenses, rent, utilities, administrative expenses, and freight. Basically, anything that you need to pay to keep your business open, but that doesn’t necessarily contribute to your product or service in a direct way.

Taxes and interest on loans aren’t listed as an operating expense, however. These will be included later on.

Operating income

Operating income is what you’ve got left over after you subtract your operating expenses from your gross margin.

Gross Margin – Operating Expenses = Operating Income

Sometimes it’s also referred to as EBITA (earnings before interest, taxes, depreciation, and amortization.)

Interest

Any interest that your company has paid on outstanding loans is included here.

Depreciation and amortization

Long-term assets like expensive pieces of machinery and equipment will gradually lose their value over time. Contrast this with smaller items like stationery, which get entirely expensed in a single year.

Calculating depreciation and amortization is an entire topic unto itself. But just know that once you calculate your depreciation and amortization, it’ll be expensed on your P&L statement here.

Taxes

Any taxes, including income tax or sales taxes paid on materials you’ve purchased, are included here.

Net profit

Net profit is the “bottom line” that you end up with after you subtract all of your expenses from your revenue. It’s also sometimes referred to as operating profit, net earnings, or net income.

If your expenses ever exceed your revenue, then you can end up with a net loss. That means you’re spending more money than you’re earning.

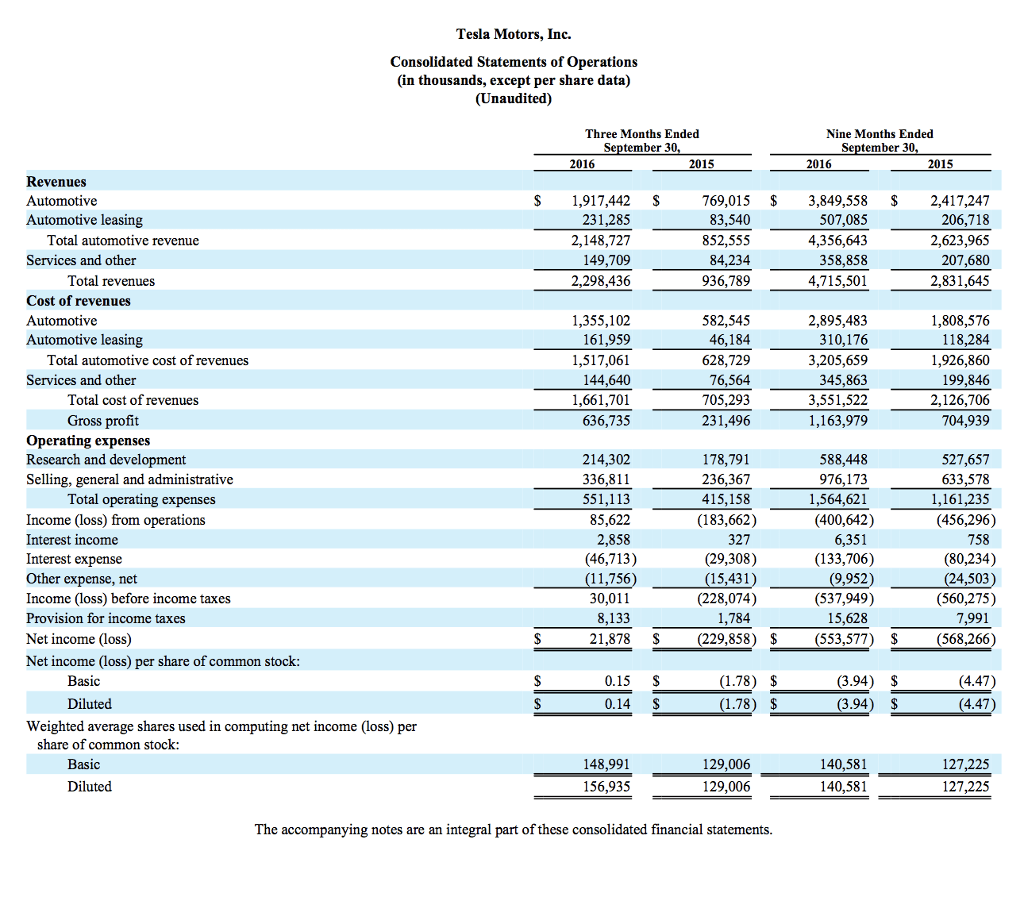

Example profit and loss statement

Below is an example of a P&L statement for Tesla Motors Inc, which they refer to as a Consolidated Statement of Operations.

How accounting principles can impact the profit and loss statement

The change to your company’s actual bank account balance at the end of the period may be very different from the bottom line (net income) listed on your profit and loss statement.

This is because of a couple of accounting principles that we need to keep in mind. They can create a difference between actual cash generated, and the amount of profit that shows on our books.

Revenue recognition principle

Businesses typically recognize revenue at the time of the sale, not necessarily when the cash gets received. This is a basic property of using an accrual accounting method instead of a cash-based system.

For example, you might sell a chair to a customer with 30-day terms.

They take the chair home right away, but they don’t pay any cash at the time of the sale. Instead, the amount is recorded on the balance sheet as accounts receivable.

So, while you’ve made the revenue right away, you won’t see the cash in your bank account until later.

Matching principle

The matching principle states that we need to match our expenses to revenues during the periods that those revenues were earned.

We briefly mentioned depreciation earlier, and this is one area where the matching principle needs to be considered.

You might buy an expensive machine for $200,000 that has an expected useful life of 10 years. This means it should be able to be used to earn revenue for the company for the next decade.

So, following the matching principle, we may expense the machine at a rate of $20,000 per year for 10 years, as opposed to deducting the entire expense in year one.

Are all companies required to prepare profit and loss statements?

Only publicly traded companies are legally required to prepare P&L statements and file them with the Securities and Exchange Commission (SEC). Currently, less than 1% of US companies are public. Only about 6,000 companies currently trade on the NYSE and NASDAQ.

Private companies aren’t required to prepare a formal financial statement, although many still do.

Financial statements, including a profit and loss statement, provide decision-makers in the company with an accurate and up-to-date summary of how the company is performing.

Take your financial knowledge to the next level

Now you know how to read a profit and loss statement, and how it can be useful.

If you’re ready to elevate your business skills and careers even further, Pareto Labs can help. Our on demand courses give you access to the business training and insider secrets that launched the careers of top CEOs and industry titans (and you’ll learn from them, too).